Is it worth insuring your classic car with a specialized insurance?

Before I go any further, I’ll advance the answer in my opinion. Radically YES.

A paradox: Despite the care that most classic car owners put into their vehicles, on several occasions I have heard or read comments where insurance for these cars is minimized. Comments like “for this car that almost does not run, do not complicate yourself, there are many cheap insurances.“. Or a few days ago I read a commentary that (literally) said: “any crappy insurance (sic) is good enough for you.“.

Insuring a classic car. Frequently Asked Questions

This is one of the headaches of many classic car owners: coverage for something as imponderable as an accident that can cause damage to a vehicle in which they have invested so much effort, hours and money.

I will summarize the topic in some frequently asked questions with direct links to the part of the post that may be of interest to you in case you prefer a quick read:

-

- Can a classic car be full-coverage insured? Yes. See here

- Is it true that the older/older the car, the more expensive the insurance? It depends on whether it is insured as a classic or not. If it is as a classic, then no. See here.

- Is classic car insurance cheap? The annual fee can be between 160 euros and 260 euros for a full-coverage insurance at agreed value. See here.

- What requirements do I need to insure my classic car? Check out here.

- What happens if I have a claim with a classic car? It depends on the insurance you have. With ordinary insurance, you will recover the venal value. With classic car specialized insurance you can recover up to the agreed market value. See here.

In any case, throughout this post, I will try to give you answers to these and other questions so that you can make the most advantageous choice.

What happens if I have an accident?

You have a classic (or additionally historic) car. And I assume you know about what is called the “venal value” of vehicles. You don’t need to be a legal expert to know what will happen if you are unfortunate enough to have a blow of a certain magnitude (caused by you or a third party) that totally or partially destroys your car. Or, without even mentioning the term “destruction”, it causes damage of a certain degree.

I would tell you that before you make any assurances, it is worth making the decision with all the information on the table.

How much is my classic car really worth? (data for Spain as of November 2023)

Here you will have at least three points of view (objective points of view, here I am going to leave out the sentimental or personal point of view, because that is subjective, and because it is not the purpose of this article)

- The insurers’ point of view: Venal value: This is the value that the company considers the vehicle to have had before the loss. And it is calculated with a depreciation table on the base price from new. And this base price, in Spain, is maintained by the Spanish Tax Administration and published in the Official State Gazette; you can download it here -it is updated every one or two years-. On this price, the insurer will calculate a percentage that decreases as the years go by. For a car 12 years old or older, the value is 10% of the base.

I give you a real example taken at random: A 2000 Audi A4 TDi. Its base price according to official tables is 25300 euros. Since it is more than 12 years old, its venal value will be something like 2500 euros.

From this calculation, consider what the venal value of a (for example) 1972 Renault 8 will be. Possibly zero, or a couple of hundred euros. It may not even exceed the cost of towing it to the scrapyard in the event of an accident.

- The market value point of view: This may seem variable but it is not so much: the classic car market has a series of prices that can be seen in any of the buying/selling portals. And, excluding the extremes, above or below, there are prices that are assumed for each model. To continue with the previous example, that Renault 8 that I mentioned before, can have a value between 4000 and 20000 euros (depending on the state and version, and obviously there are more expensive units if they are very exclusive as there are cheaper if they are to restore).

- How much was your real cost: I am referring to objective costs of restoration, repair, overhaul. If you have a classic, I don’t need to give you many details because you will know it. If you count spare parts, upholstery, bodywork, paint – here it depends on how far you have gone with the restoration/reconditioning – the list can easily add up to a few thousand euros over time.

How much will I recover in the event of a claim? The term nobody wants to hear: "Total loss".

With a standard “modern car” insurance: You will recover the venal value. So if the repair of your Renault 8 If the cost of the accident is more than a couple of hundred euros -which is the most you can aspire to as venal value-, the company will consider it a total loss, will pay you those 200 euros and will even “do you the favor” of letting you take the remains home.

- There is an important nuance to mention here: Some companies sometimes have some product that extends the aforementioned “venal value” under certain circumstances. But, in any case, I would tell you not to expect major improvements. I, at least, have never encountered them.

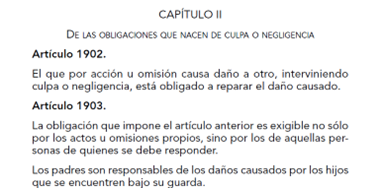

In any case, if you disagree with your “verdict” of “total loss” and the pitiful compensation you will receive -which, as I said, may literally not even cover the towing costs- you can sue the company to claim a compensation according to the market price. You could use the Spanish Civil Code (article 1902) which states that “The one who by action or omission causes damage to another, intervening fault or negligence, is obliged to repair the damage caused..”

You can see it here on page 452 of the document.

The problem is that, in order to do so, you will have to proceed through the courts -at least in Spain-, so you will probably have lawyer’s fees (plus attorney’s fees -for Spain- if the claim exceeds 2000 euros, which will certainly be the case).

In the end it will be a judge who will arbitrate a solution/amount that may or may not meet your needs/expectations.

Not to mention the emotional, time, and energy drain on the entire journey.

What is clear is that you don’t want the several thousand euros you have put into your classic car to end up as a pile of scrap metal and a 200 euro “tip” because of an accident for which you are not guilty.

How can you avoid all this? Take out a classic insurance policy.

This situation I have described above of “what happens if my classic car is destroyed in an accident for which I am not at fault?” is very common: I honestly do not know right now how many classic/historic cars there are in Spain, but there are a few thousand. There are many people in the same situation.

This is why there are several companies that offer a specialized product for classic cars. And they do cover an agreed value in the event of a loss (with or without fault). In other words: You can take out full-coverage insurance for your classic at the agreed value.

And the prices are extremely reasonable. This is based on the fact that the accident rate of classic cars is very low, mainly due to three factors:

- They do very few kilometers per year.

- They are very well cared for by their owners, both in terms of maintenance and driving.

- Most of the time -if not all- they avoid driving in “conflictive” accident areas/times, such as belts around big cities, rush hours, etc.

At the time of writing this post, there are two companies or brokerages for which we have direct reference.

- ROMAGOSA – Insurance for classic cars. You can find them here: https://www.seguroparatuclasico.com/

- COTER – They have a rate for classic and/or historic cars. You can find them here: https://seguroscoter.com/

In Spain, and most countries, there are obviously more of them. You can Google and you will find many. But I mention these two because I have direct references that they are what they say they are and they work. I know the first one because it is where we have our vehicles insured, and the second one because it is endorsed by the Renault 4CV Friends Club which is currently the largest entity in Spain around this model (about 800 members/registered Renault 4CV vehicles).

What do they ask for and what do they offer? How much do these classic car insurances cost?

Here I am going to give you some concrete figures of what they can ask and offer you (if I didn’t give you this information, this article would make little sense 😊). So here we go:

- Requirements:

- The car is a classic/historic car (usually using the 25 years as the yardstick for estimating classic status).

- The car must NOT have visible defects in the sheet metal and/or paintwork:

- That the car is cared for and in good appearance in terms of interiors, engine, etc.

- The car “sleeps” in the garage

- No more than a few kilometers per year (5000 or 10000 depending on what is agreed).

- That the drivers are declared.

- That it has the Tecnical check up to date (or if it does not, that you sign a commitment to pass it in the coming days -usually 15 days-.

- Some may require that the declared driver be “outside” the risk zone (under 20 years of age or over 75, less than 2 years of driving license, etc.).

- What they offer:

- A typical third party insurance for civil liability, roadside assistance, etc. etc. (so far the usual).

- FULL COVERAGE or COMPREHENSIVE INSURANCE: Depending on the particular conditions of each company. In summary:

- ROMAGOSA:You agree on a value of the car, which the company will corroborate/adjust according to the market price (and NOT the venal value). That value will be the maximum you can get to repair/replace your damaged car.

- COTER: For cars prior to 1965 a replacement value in case of total loss between 15.000 and 90.000 euros depending on the supplement you pay (ranging from 35 euros to 85 euros as of November 2023).

As I said, there are more companies, but I am mentioning these two because I have references of them.

How much does a classic car full-coverage insurance cost?

I will give you a couple of real examples (Spain as of November 2023 with ROMAGOSA, for a driver with maximum no-claims bonus):

- An MGA (1961) with replacement/repair value up to 32.000 euros: 240 euros/year

- A Renault Dauphine Gordini (1963) with a replacement/repair value of up to 12.000 euros: 170 euros/year.

NOTE: These FULL COVERAGE INSURANCES have an excess of 600 euros. There may also be some cases in which the agreed value is somewhat lower than the market value or what you have invested in the car. But I would suggest you look at it in the following way:

Excess: These insurances are not intended for you to repair minor damage.

Agreed value: Although the agreed value may be slightly lower than what you consider for your particular unit, you can look at it as

-

-

- You do NOT take out insurance to get rich by replacement at the expense of a potential claim (which is against the law).

- The replacement values will more than cover repairs even in the event of “major” damage to the car. In other words, and as an example, in the case of the Renault Gordini, you could “show up” at the body shop with a repair of 10.000 euros (which is already a major repair) knowing that your insurance covers it.

-

Conclusion.

Classic car owners take exquisite care in their units. Some are true jewels, automotive icons or living testimony to the industrial history of the country in which they live.

Insuring such a vehicle in good condition can be the difference between being able to keep it forever or having its life end suddenly due to someone else’s carelessness in a parking lot or at an intersection of two streets.